Assets

+ New Loan

£100,000

Liabilities

+ New Deposit

£100,000

Bank deposits vs central bank money

How banks create money through lending

The UK's institutional architecture

The Consolidated Fund mechanism

What they actually do

The accounting identity that connects all sectors

Real vs perceived constraints

Duration

40 min

Presentation followed by Q&A. Technical appendix with detailed accounting tables available.

Part One

Bank of England, December 2013

When we talk about "money" in the economy, we're overwhelmingly talking about numbers in bank accounts — not physical cash.

The composition of UK broad money:

Bank deposits (commercial bank money): 97%

Currency (notes and coins): 3%

This means understanding money creation requires understanding how these bank deposits come into existence.

Source: Bank of England (2014) "Money creation in the modern economy", Quarterly Bulletin Q1

Fact: 97% of the money we hold is commercial bank deposits.

But this is a stock measure — it tells us what type of money people hold today, not how that money came into existence.

Commercial Bank Lending

When banks make loans, they create matching deposits. This is a major source of money during economic expansions.

Government Spending

Every payment from HM Treasury increases deposits in the commercial banking system. Government deficits are therefore a second source of money creation.

Money issued by the Bank of England

Includes:

• Physical currency (notes & coins)

• Reserves (bank accounts at BoE)

Who holds it: Banks hold reserves; public holds currency

Money created by commercial banks

Includes:

• Current account balances

• Savings account balances

Who holds it: Households, businesses, non-bank financial institutions

Ultimate Authority

Parliament

Power to tax • Consolidated Fund

Monetary Authority

Bank of England

Issues reserves & currency • Settles between banks

Money Creators

Commercial Banks

Create deposits through lending • Hold accounts at BoE

Money Users

Households, Businesses, Non-Bank Financial Institutions

Hold bank deposits • Use money for transactions

Each layer's money is an IOU convertible into money from the layer above.

Adapted from Bell (2001) "The Role of the State and the Hierarchy of Money"

Part Two

"Banks collect deposits from savers and then lend those funds to borrowers..."

🏠

Savers

🏦

Bank

(intermediary)

👤

Borrowers

— Bank of England, Quarterly Bulletin 2014 Q1

Saving does not increase the deposits or 'funds available' for banks to lend.

When a bank makes a loan, it simultaneously creates a matching deposit:

Assets

+ New Loan

£100,000

Liabilities

+ New Deposit

£100,000

Assets

+ Bank Deposit

£100,000

Liabilities

+ Loan Owed

£100,000

This is sometimes called "fountain pen money" — created at the stroke of a banker's pen.

"The central bank controls the money supply by setting the quantity of reserves, which banks then 'multiply up'..."

Central Bank

£100

reserves

Multiplier

10x

(if 10% reserve ratio)

Money Supply

£1,000

deposits

Reserves don't constrain lending

Banks decide how much to lend based on profitable opportunities. They obtain reserves afterwards.

No binding reserve requirements

The UK has no reserve ratio requirement. The BoE supplies reserves on demand to meet settlement needs.

Central banks set interest rates, not the quantity of money. Reserves follow lending, not the other way around.

Banks can't create unlimited money. Three sets of constraints limit money creation:

• Profitability in competitive market

• Capital constraints and risk assessment

• Liquidity and funding management after lending (not a prerequisite to lend)

• Willingness to borrow

• Loan repayments destroy money

• "Reflux" of unwanted money

• Interest rates affect loan demand

• Prudential regulation (capital, liquidity)

• Ultimate constraint

Source: Bank of England (2014) — see also Farag, Harland and Nixon (2013) on capital and liquidity requirements

"Most of the money in circulation is created, not by the printing presses of the Bank of England, but by the commercial banks themselves."

— Bank of England (2014)But what about government spending? How does the state create and inject money into the economy?

Part Three

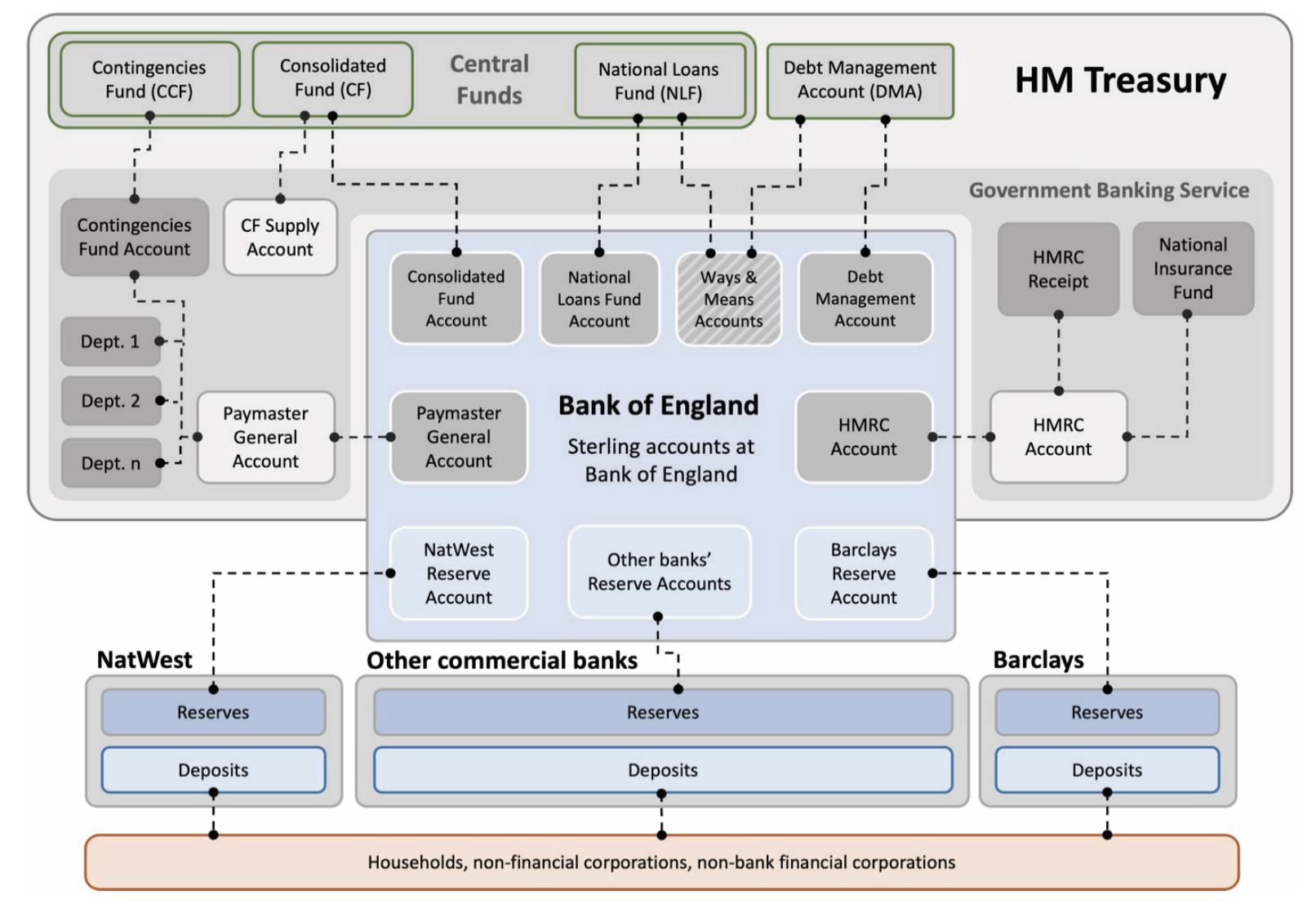

The UK's institutional architecture

The core legal and accounting structure at the heart of UK public finance

Established 1787

"One fund into which shall flow every stream of public revenue, and from which shall come the supply for every service"

— HM Treasury (2024)

What it does:

• Origin of all departmental expenditures

• Source of government securities issuance

• Destination for most government revenue

The Central Funds

Consolidated Fund

“Current account”

National Loans Fund

Lending & borrowing

Contingencies Fund

Urgent expenditure

Governed by Exchequer and Audit Departments Act 1866, National Loans Act 1968

Source: Berkeley et al. (2025), Figure 1

Source: Berkeley et al. (2025)

Part Four

What they actually do

Part Five

The accounting identity that connects all sectors

Use ↓ to see other countries

Large government deficits matched by large private surpluses

Government deficits fund both private surpluses and current account deficits

Export surpluses allow lower government deficits

Constrained by Eurozone fiscal rules?

Wars historically drove debt accumulation; peacetime growth and inflation reduced debt ratios

Part Six

Real constraints vs perceived constraints